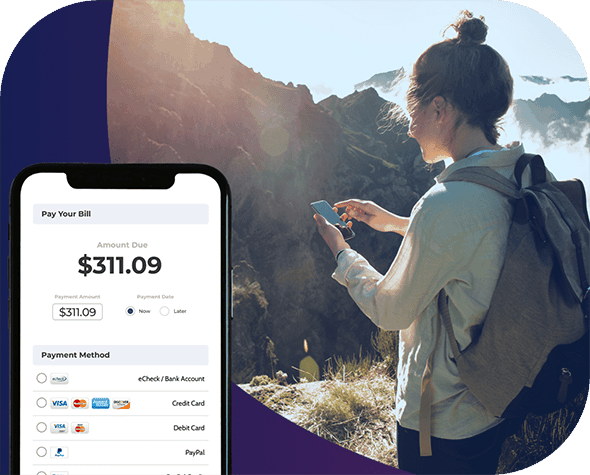

Bring Modern Money Movement and Payments to Your Platform

Powered by today’s only integrated real-time digital bill presentment, payment and money movement network, see how we’re transforming bill management and payment, loan repayment and real-time money movement to put your customers in complete control of their finances.